Thailand: Legal Update: Updated Social Security Contribution Wage Base and Enhanced Benefits under Section 33

We published a newsletter regarding Updated Social Security Contribution Wage Base and Enhanced Benefits under Section 33 in Thailand. To view PDF version, please click the following link.

→Legal Update: Updated Social Security Contribution Wage Base and Enhanced Benefits under Section 33

Legal Update:

Updated Social Security Contribution Wage Base and Enhanced Benefits under Section 33

27th February 2025

OAL Thailand Office

On 11th December 2025, the Ministerial Regulation Prescribing the Minimum and Maximum Wages Used as the Basis for Calculating the Contributions of the Insured Person under Section 33 B.E. 2568 (2025) (the “Wage Base Regulation B.E. 2568 (2025)”) was published and became effective on 1st January 2026. This Wage Base Regulation B.E. 2568 (2025) repeals the Ministerial Regulation No. 7 B.E. 2538 (1995) (the “Previous Regulation”) to increase the maximum base wage used to calculate contribution payments to the Social Security Fund (the “SSF”). This amendment is intended to ensure that contribution calculations for insured persons under Section 33 of the Social Security Act B.E. 2533 (1990) (“SSA”) better reflect current economic conditions.

1. Overview and Scope of the Regulation

The Wage Base Regulation B.E. 2568 (2025) applies to contributions made by insured persons under Section 33 of the SSA. Under Section 33, every employee is required to be an insured person, and under Section 46, both the insured employee and the employer must pay contributions to the SSF at the rates prescribed in the relevant ministerial regulations. These contributions are not calculated based on the employee’s actual total wages received but are calculated based on the wage base prescribed by law.

2. Key change: Increment of maximum base wage

Under the Previous Regulation, the wage base was between THB 1,650 and THB 15,000. The Wage Base Regulation B.E. 2568 (2025) replaces this with a tiered wage base system under which the maximum wage base will be gradually increased. With the current contribution rate set at 5% of the base wage, the contributions may be compared as follows:

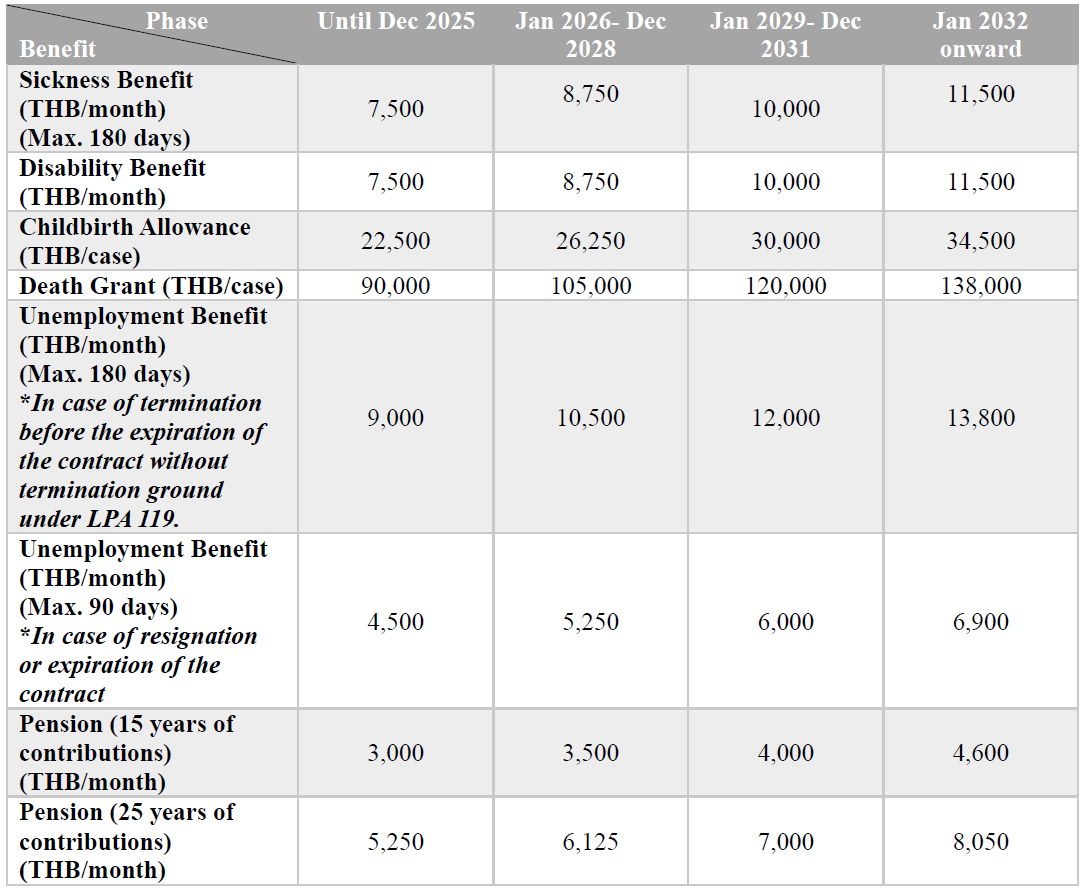

3. Benefit Increment

Insured persons are entitled to seven types of benefits from the SSF. The wage base used to calculate these benefits is the same wage base used to calculate contributions of insured persons under Section 46.

Accordingly, the increase in the maximum wage base used for calculating contributions will also result in higher benefit ceilings for insured persons, as outlined below.

4. Legal Obligations and Penalties

The employer is responsible for submitting both the employer’s and the employee’s contributions to the Social Security Office by the 15th of the month following the month in which wages are paid. If the employer fails to make the payment within the prescribed period, the employer must pay an additional surcharge at the rate of 2% per month on the outstanding contribution amount.

5. Business Implications

A revised wage ceiling for social security contributions takes effect on 1st January 2026. From that date onward, employers are responsible for applying the new threshold to all relevant payroll calculations and for ensuring timely remittance of both the employer and employee portions of the contribution.

6. Conclusion

To conclude, employers must adjust their payroll processes to comply with the new standards and ensure that employees are informed about the updated social security benefits. This proactive adjustment supports legal compliance, reduces the risk of potential liabilities arising from non-compliance, and helps ensure that all employees can fully access their entitled social security benefits without disruption.

Should you have any questions or require further clarification, please do not hesitate to contact One Asia Lawyers (Thailand Office), where our team will be pleased to assist you.