Philippines: SEC Adopts Internationally-aligned Reporting Standards and Guidelines on Sustainability and Climate-related Disclosures

We published a newsletter regarding SEC Adopts Internationally-aligned Reporting Standards and Guidelines on Sustainability and Climate-related Disclosures in the Philippines. To view PDF version, please click the following link.

SEC Adopts Internationally-aligned Reporting Standards and Guidelines

on Sustainability and Climate-related Disclosures

March 2026

One Asia Lawyers Philippines Team

(Philippines) Atty. Razel Ann P. Esteban

(Japan) Lawyer Yasuaki Nanba

I. Overview

On 22 December 2025, the Securities and Exchange Commission (SEC) issued Memorandum Circular No. 16, series of 2025, adopting the Philippine Financial Reporting Standards (PFRS) S1 – General Requirements for Disclosure of Sustainability-related Financial Information, and PFRS S2 – Climate-related Disclosures, which correspond to the International Financial Reporting Standards (IFRS) S1 and S2, issued by the International Sustainability Standards Board (ISSB). The SEC also promulgated accordingly the Sustainability Reporting Guidelines for publicly listed companies (PLCs) and large non-listed entities (LNLs), which includes the PFRS Adoption Roadmap.

The Guidelines aim to encourage sustainable business practices and align company disclosures with international standards to attract environmental, social, and governance (ESG)-focused investors in the Philippines. With these new reporting guidelines for the adoption of the PFRS, SEC Memorandum Circular No. 4, series of 2019, which previously promulgated the Sustainability Reporting Guidelines for PLCs, has now been repealed.

The salient points under the new Circular are summarized below:

II. Covered Entities

Previously, only PLCs are required to submit a Sustainability Report alongside their annual reports, in accordance with SEC MC No. 4-2019. With the new Circular, both PLCs and LNLs are now required to submit a Sustainability Report. A company qualifies as an LNL if its annual revenue for the fiscal year ending on or after 31 December 2027 is more than Php 15 billion. If the LNL is also required to report under Sec. 17.2 of the Securities and Regulation Code, namely, it has assets worth at least Php 50 million, has a minimum of 200 stockholders, and the stockholders own at least 100 shares each, it is required to submit their Sustainability Report alongside their annual reports just like PLCs. Other LNLs who do not fall under this category are to submit their Sustainability Reports alongside their audited financial statements. The Sustainability Reports of both PLCs and LNLs must be reviewed and approved by their Board of Directors.

III. Applicable Framework

The Sustainability Reporting Guidelines under SEC MC No. 4-2019 built upon 4 globally-accepted frameworks, namely, the Global Reporting Initiative (GRI) Sustainability Reporting Standards, the International Integrated Reporting Council’s (IIRC) Integrated Reporting (IR) Framework, the Sustainability Accounting Standards Board (SASB) Sustainability Accounting Standards, and the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

In the new Circular, the Philippines formally adopted the Philippine Financial Reporting Standards (PFRS) S1 and S2, which are locally adopted versions of the International Sustainability Standards Board (ISSB) standards S1 and S2. The new Circular allows the inclusion of other disclosures aligned with other international standards and frameworks in the Sustainability Report as an addition to PFRS S1 and S2, provided that the disclosure does not obscure material information and the framework applied does not conflict with the PFRS S1 and S2 and is disclosed in the report.

IV. Transition and Implementation

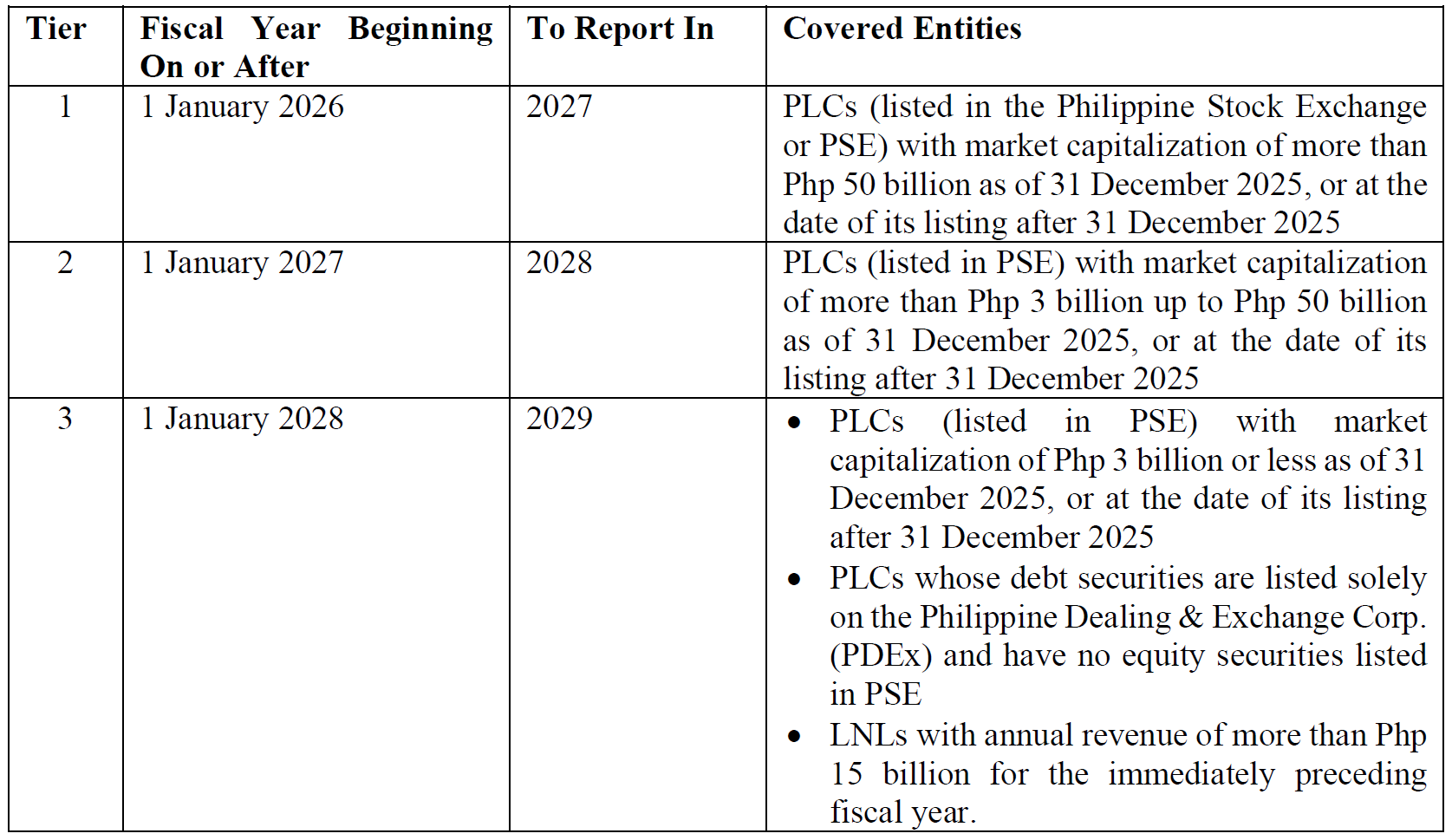

Under the new Circular, PLCs are to continue with the Sustainability Reporting Guidelines prescribed under SEC MC No. 4-2019 only up until the fiscal year prior to their mandatory adoption of the PFRS. Beginning in the fiscal year 2026, PLCs and LNLs are required to start adopting PFRS S1 and S2 under a tiered approach as follows:

The tiered approach is only to determine the timing of the first adoption of PFRS S1 and S2. Once classified, the covered PLCs and LNLs are to prepare and submit an annual sustainability report on an ongoing basis.

V. Mandatory External Assurance

Under SEC MC No. 4-2019, PLCs were not required to obtain external or third-party assurance. In the new Circular, covered entities must now obtain limited external assurance on their Scope 1 and Scope 2 greenhouse gas (GHG) emissions from an independent practitioner (either a Certified Public Accountant or qualified public non-accountant) 2 years after the initial implementation of PFRS S1 and S2 as provided above, thus:

- Tier 1 entities – In 2028

- Tier 2 entities – In 2029

- Tier 3 entities – In 2030

Over time, the requirement will progress toward reasonable assurance. The external assurance is required to be conducted in accordance with the International Standard on Sustainability Assurance (ISSA) 5000.

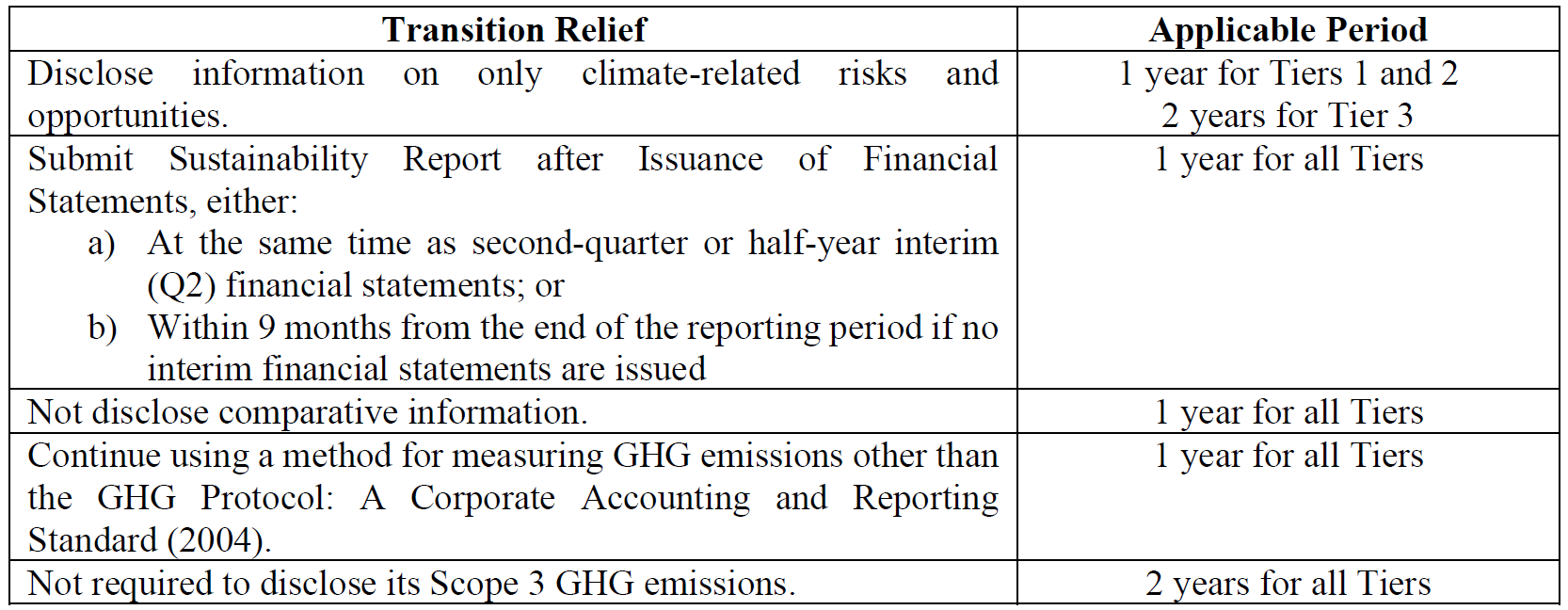

VI. Transition Reliefs

SEC MC No. 4-2019 previously implemented a “comply or explain” approach, in which PLCs, for the first three years of effectivity of the MC, are required to attach the Sustainability Report to their Annual Reports but they can provide explanations for items in which they still have no available data.

Under the new Circular, limited extensions have been provided to the following transition reliefs under the Standards:

VII. Exemptions

The new Circular introduced an exemption for LNLs, providing that they may be exempted from the mandatory reporting requirement if all the following conditions are met:

- Its immediate, intermediate or ultimate parent company is already preparing and filing the prescribed Sustainability Report in accordance with the sustainability reporting framework prescribed in the jurisdiction where such parent company submits its corporate reports;

- Its sustainability-related disclosures are included in the parent company’s publicly-available report; and

- It submits a duly accomplished Certificate of Exemption from Mandatory Sustainability Reporting as an attachment to its audited financial statements.

VIII. Penalties

SEC MC No. 4-2019 previously only penalized PLCs who did not attach their Sustainability Report to their Annual Report. The New Circular now penalizes both the non-submission of the Sustainability Report as well as non-compliance with the PFRS S1 or S2. PLCs who are non-compliant shall be subject to the same penalties as Incomplete Annual Report in accordance with SEC Memorandum Circular No. 6-2005 (provided below) as well as SEC Resolution No. 581, series of 2021, which provides that the penalties for non-submission or late submission of Sustainability Reports shall be subject to a separate scaling of penalties:

Given the adoption of the PFRS S1 or S2, there shall be a fresh count of offenses under the new Circular, and shall not continue from prior offenses under SEC MC No. 4-2019.

For LNLs, the SEC shall issue subsequent issuances for their applicable penalties.

IX. What Should Companies Do?

Foreign companies which are publicly-listed companies or are considered large non-listed entities in the Philippines must ensure that it complies with the Philippine Financial Reporting Standards S1 and S2 and timely prepare and submit their Sustainability Reports within the designated fiscal year based on their classified tier. In particular, foreign PLCs under Tier 1 are already mandated to adopt the PFRS S1 and S2 starting 1 January 2026 and should align their company disclosures with the Standards as soon as possible, since they will be required to submit their Report in 2027. Covered foreign companies must also ensure that their greenhouse gas emissions are audit-ready within 2 years after their implementation of the PFRS.